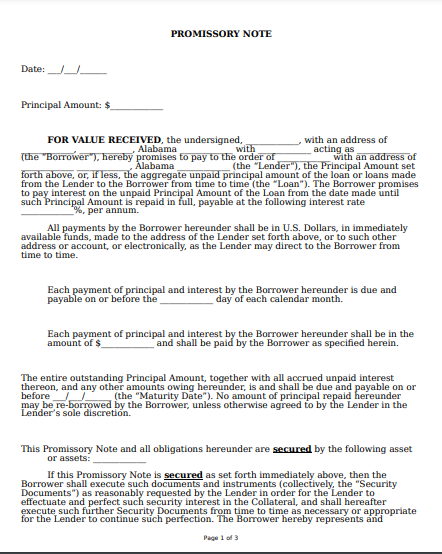

What Is a Promissory Note?

A promissory note is a legally binding agreement containing a written promise to pay back a specific amount of money within a specified period or on-demand. The parties to a promissory note are a borrower who receives the money and a lender who provides the money to the borrower.

A promissory note sets out all the terms and conditions relating to debt, such as payment schedule, interest rate, collateral security, due date, and penalty if the borrower defaults.

When to Use a Promissory Note?

Promissory notes are important to ensure that money borrowed is paid back. They act as essential documents of record to hold the borrower accountable for the money due and provide protection to the lender against non-payment. By agreeing to all the terms and conditions in advance, the parties avoid chances of future disputes or ambiguities.

Promissory notes can be used for various purposes. Some of the common purposes for which they are used are:

-

Real estate sell-purchase, real estate down payments, or real estate mortgages.

-

Loans of personal nature between family members, friends, or colleagues.

-

Students loans for tuition fees and college expenses.

-

Business and commercial loans.

-

Car, automobile, or vehicle loans.

Secured vs. Unsecured Promissory Note Form

A promissory note can be secured or unsecured.

Secured. A secured promissory note provides collateral security in the form of real assets such as a house or car as a remedy against failure to pay. If the borrower defaults, the lender can seize the property to obtain repayment of the loan. A lender must ensure that the property specified in a secured promissory note is of sufficient value to cover the principal plus the interest in case of default. If the borrower undergoes bankruptcy, then the lender's right to claim a repayment from the specified property will come before the right of other unsecured creditors.

Unsecured: An unsecured promissory note does not provide any collateral security as a remedy against failure to pay back. If non-payment by the borrower occurs, the lender will have to file a lawsuit in court to recover the loan from the borrower. If the borrower undergoes bankruptcy, then the lender will have no preferential right over other unsecured creditors.

A lender is recommended to use a secured note while lending money to have extra safety.

There is also a promissory note for a car sale explicitly designed for vehicle purchase. It acts as a promise to pay out a car loan and records the key transaction details.

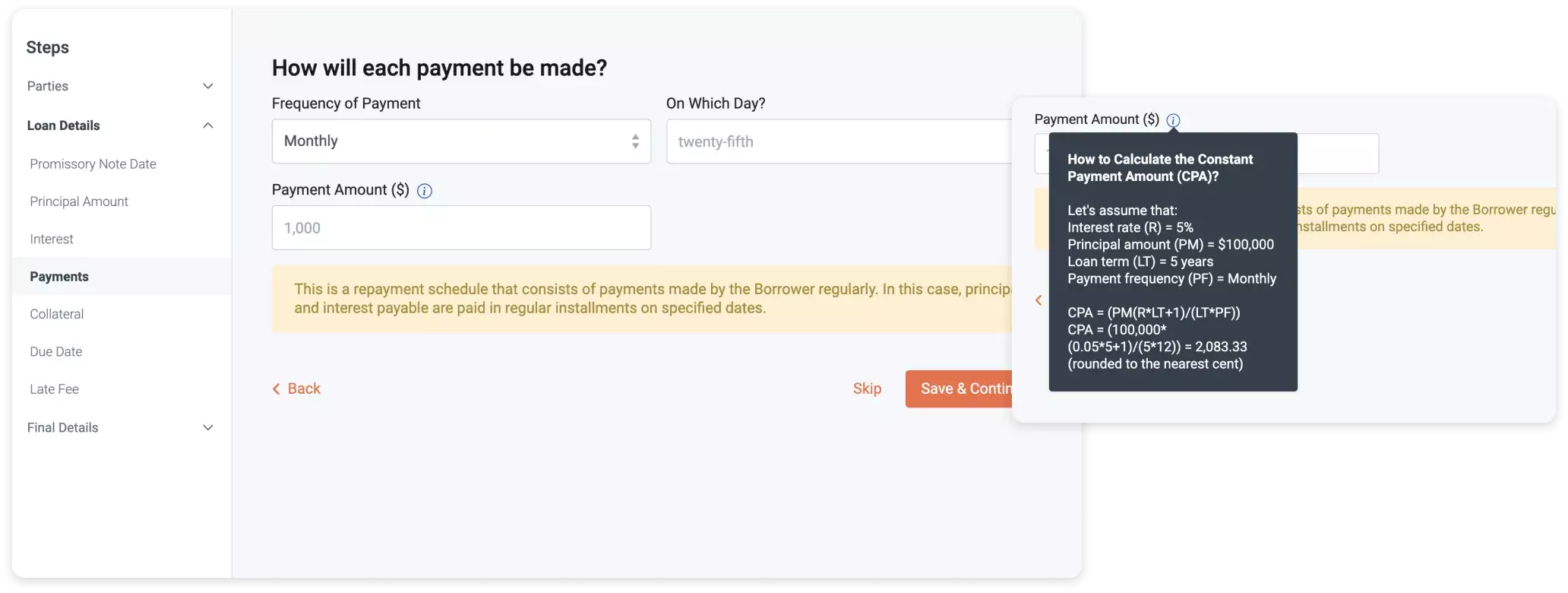

What Payment Options Are Available with a Promissory Note?

Payment is typically first applied towards the interest payable and then the loan amount. The note should also specify late fees, either a flat fee or a percentage of the amount due for missed due dates. The lender can issue a demand letter informing the borrower that he has missed his due date and needs to pay late fees. The note should specify the time period after which late payment will be considered as default. There are four main payment options available with a promissory note.

Regular Installment Payment: Principal and interest payable are paid in regular installments on specified dates.

Installment with Final Balloon Payment: Interest payment is made in regular installments, and the principal amount is paid on the maturity date.

Lump-Sum Payment: The total amount, including the interest accrued and the principal amount, is paid on the maturity date.

Payable on Demand: No specific due date is provided, and the borrower has to pay back the lender whenever demanded by the lender.

Amortization: This is used for long-term loans by creating a payment schedule. The schedule is created so that the payment towards interest keeps decreasing over time, and the payment towards the principal keeps increasing over time.

Steps to Creating a Promissory Note

A promissory note is an important legally binding document, considering, of course, it is written correctly. But the good news is that it's much shorter and less complicated than most agreements. Hence, there's no need to hire a law firm or have a law degree to create this document.

With the help of our form and instructions, you can complete your promissory note in under ten minutes. You can also use our document builder that will lead you step-by-step to your personalized document in no time.

Step 1. Mutual Agreement

Before formally writing the agreement, the parties should sit down and mutually agree upon all terms verbally. They should discuss and agree upon terms relating to the loan amount, interest rate, payment plan, late fees, security, default, and co-signer. This will ensure that each party knows, understands, and agrees to all the terms in the same sense.

Step 2. Background Check

It is always advisable to do a background check on the opposite party. A lender should run a credit check to find out if the borrower has other outstanding debts. A lender should also know if there is any other claim or mortgage on the collateral. Before doing the credit check, the lender must obtain a written authorization from the borrower to do the same. Equifax, Experian, and TransUnion are some of the reputed credit reporting agencies. Similarly, a borrower should also make sure that the money given legally belongs to the lender.

Step 3. Collateral and Co-signer

Parties should specifically identify the collateral and the co-signer if they decide to include them. They should also discuss the value of the asset to be provided as security. The person who will be the co-signer should be informed about all the terms, and his consent should be obtained beforehand.

Step 4. Writing the Promissory Note

After following the steps mentioned above, parties should meet, write, and sign the agreement. Loan money should be given to the borrower after signing.

Step 5. Loan Release

After the borrower has made payments in time and accordance with the promissory note, the lender should sign a loan release form. The loan release form will certify that repayment has been made following the agreement. It will relieve the borrower from any further liability.

Frequently Asked Questions

What makes a promissory note invalid?

A promissory note can become unenforceable under the law in the following cases:

-

If it’s not written correctly.

-

If the borrower does not sign the note.

-

If the interest rate exceeds the maximum limit under the state law.

-

If the note is altered without mutual agreement.

-

Notes with ambiguous terms, such as unclear dates or missing party details, can also become invalid.

Additionally, a promissory note is a contract. Like any other contract, it should fulfill all requirements of a valid contract, such as minimum legal age of the parties, soundness of mind, and legal objective.

Is it possible to sell or transfer my note?

Yes, lenders can sell, transfer, and even use their notes as a substitute for money. Notes can be transferred between lenders. When a lender wants liquidity and does not want to endure the risk of a long-term loan, he or she can sell the note to reputed note buying companies at a discount. Notes can also be transferred between family members and friends to offset another loan.

However, the law varies from state to state regarding transferability. It is crucial to keep proper records of the note and include clear language in the note to enable the note's selling or transferability. The note should include the terms "payable to order" or "payable to bearer."

What to do if the borrowed money is never paid back?

If the note is secured, then the lender can obtain the borrower's property under the loan contract. The lender will typically have to file a lawsuit to get foreclosure rights on the collateral legally. If the note is unsecured, then the lender can seek repayment through Small Claims Court. Small claims are usually limited to loans of $10,000 or less depending on the state law.